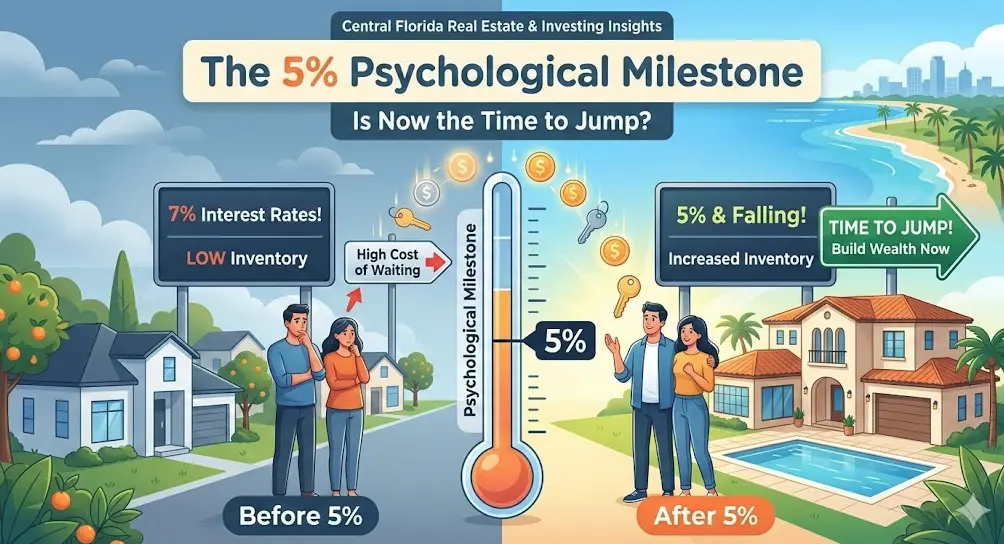

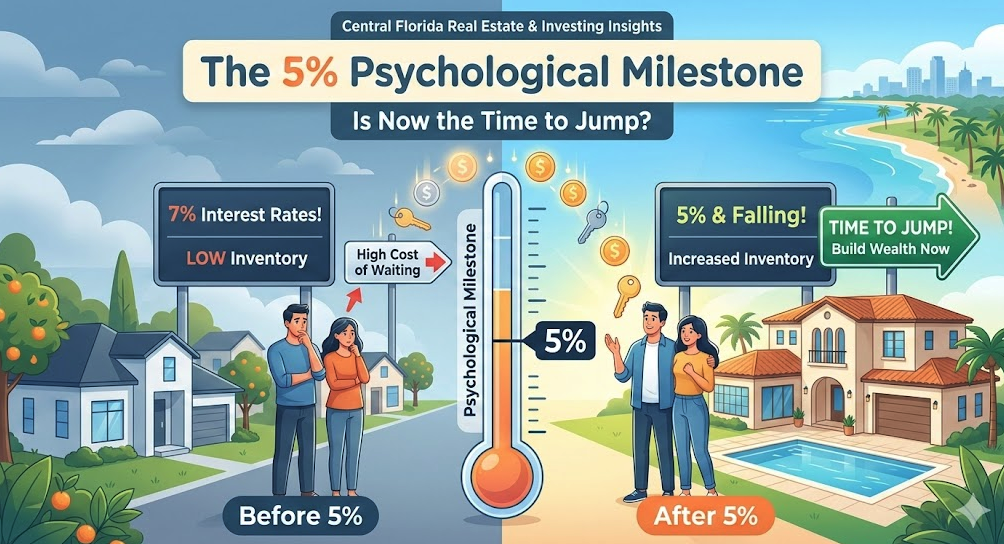

The 5% Psychological Milestone: Is Now the Time to Jump?

In the world of real estate, numbers tell a story, but psychology drives the action. For the past few years, the "7% era" of mortgage rates felt like a heavy anchor for both first-time homebuyers and seasoned investors. But as the market shifts, we are approaching a critical threshold: the 5% range.

In Central Florida—from the booming suburbs of Lake Nona to the vacation rental hotspots of Kissimmee—the 5% mark is more than just a data point. It is a psychological green light. But if everyone waits for the light to turn green at the exact same time, the road gets crowded fast.

1. Understanding the "Rate Lock" Effect

For the last several years, many homeowners in Florida have been "locked in" to rates between 2.5% and 4%. This created a supply desert. Owners were hesitant to trade a 3% rate for a 7% rate, even if their family was outgrowing their current home.

As rates dip toward 5.5% or 5%, that "gap" narrows. The psychological pain of giving up a low rate diminishes when the new rate feels "reasonable" rather than "punitive."

The Fact: Historically, the average 30-year fixed mortgage rate in the U.S. from 1971 to 2023 has been approximately 7.74%. Looking at it through this lens, a 5% rate isn't just "okay"—it's objectively excellent.

2. The Central Florida Context: Inventory vs. Demand

Central Florida is unique. Unlike stagnant markets in the Rust Belt, Florida continues to see massive net migration. According to the Florida Realtors® data, the Orlando-Kissimmee-Sanford MSA remains one of the fastest-growing regions in the state.

-

The Scenario: When rates hit 5%, the "sideline buyers" (those who have been renting and waiting) will flood the market.

-

The Risk: In real estate, price and rate often have an inverse relationship. When rates drop, buyer competition spikes, which leads to multiple-offer scenarios and price appreciation.

Example: Imagine a home listed in Winter Garden for $500,000. At a 7% rate, your monthly principal and interest is roughly $3,326. At 5%, that drops to $2,684. That $642 monthly savings is massive—but if 20 other buyers are also chasing that home and bid the price up to $550,000, your savings are quickly eroded by the higher loan amount.

3. The Investor’s Perspective: The Return of the Cash Flow

As an investor, the 5% milestone is the "Buy" signal for long-term holds. In the Orlando market, high interest rates have made it difficult for traditional long-term rentals to "pencil out" with 20% down.

When debt service decreases, the Debt Service Coverage Ratio (DSCR) improves. For investors using DSCR loans, the move from 7% to 5.5% can be the difference between a property that breaks even and one that generates $400/month in passive cash flow.

4. Why "Marry the House, Date the Rate" is Actually True Now

You’ve heard the cliché, but in the current Central Florida climate, it carries weight. If you buy now—while rates are still hovering slightly above that 5% milestone—you have less competition. You can often negotiate for Seller Concessions.

In 2026, we are seeing more sellers willing to contribute toward a 2-1 Rate Buydown. This allows you to "buy" your way into that 5% psychological milestone today, while others are still waiting for the national average to drop.

Pro Tip: If you wait until the headlines scream "RATES HIT 5%!", you lose your leverage to ask for repairs or closing costs. You’ll be too busy fighting off five other offers.

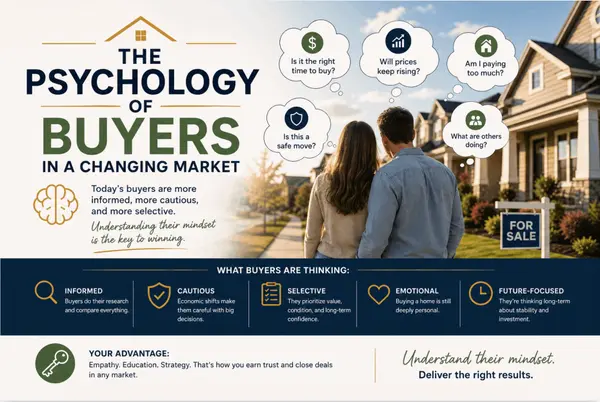

5. The Opportunity Cost of Waiting

The biggest mistake buyers make is focusing solely on the interest rate while ignoring Equity Growth. Central Florida property values have shown incredible resilience. If you wait 12 months for rates to drop by 1%, but home prices in Clermont or St. Cloud rise by 5% in that same timeframe, you’ve essentially lost money.

-

Fact: Real estate is a hedge against inflation. Even at a 5% or 6% interest rate, you are paying down your own principal rather than your landlord's mortgage.

-

The Math of Waiting: A $450,000 home that appreciates at a modest 4% will cost you $18,000 more next year. Is the potential 0.5% rate drop worth the $18,000 price hike? Usually, the answer is no.

Conclusion: Is it Time to Jump?

The "5% Psychological Milestone" is a powerful motivator, but savvy Central Florida residents know that the best time to buy is often just before the crowd reaches that milestone.

By jumping in now, you secure the asset at today's price, keep your negotiation leverage intact, and position yourself to refinance if rates continue to trend downward. Whether you are looking for your forever home in Dr. Phillips or an investment property near the attractions, the window of opportunity is widest before the rush.

Categories

Recent Posts

ARE YOU LOOKIING TO SELL YOUR HOME FOR TOP DOLLAR? CLICK THE BUTTON BELOW TO GET STARTED

SELL YOUR HOME